I cut our variable household spending by 18% in three months, and it wasn’t because I started tracking every cent in a spreadsheet. It was because I changed how we pay for things.

I run a resale business, so I’m dealing with money and transactions all day—but somehow our personal spending still slipped. Managing a family in 2026 isn’t cheap. Between groceries, gas, and keeping a 4-year-old entertained, the money just seems to evaporate. I realized that for us, credit cards had removed just enough friction that we stopped paying attention—and that’s where the leak started.

I call it “Swipe Anesthesia.” Tapping a card removes just enough awareness that you stop caring about the price. By the time I checked our bank account at the end of the month, we’d already blown a few hundred on stuff we don’t even remember buying.

The Proof: $9,000 Back in Our Pocket

I stopped guessing and started using physical cash for our daily life. Here’s what happened to our monthly variable spending (food, gas, and fun):

- Before: $4,200/month

- After: $3,450/month

- The Result: $750/month back in our pocket. That’s $9,000 a year without anyone taking a second job.

Nothing else changed—same income, same bills.

The biggest drops came from the two areas that usually kill a family budget: eating out (down 35%) and those quick impulse buys at the store (down 60%). We don’t actually need half the stuff that ends up in the cart when we have to count out physical twenties to pay for it.

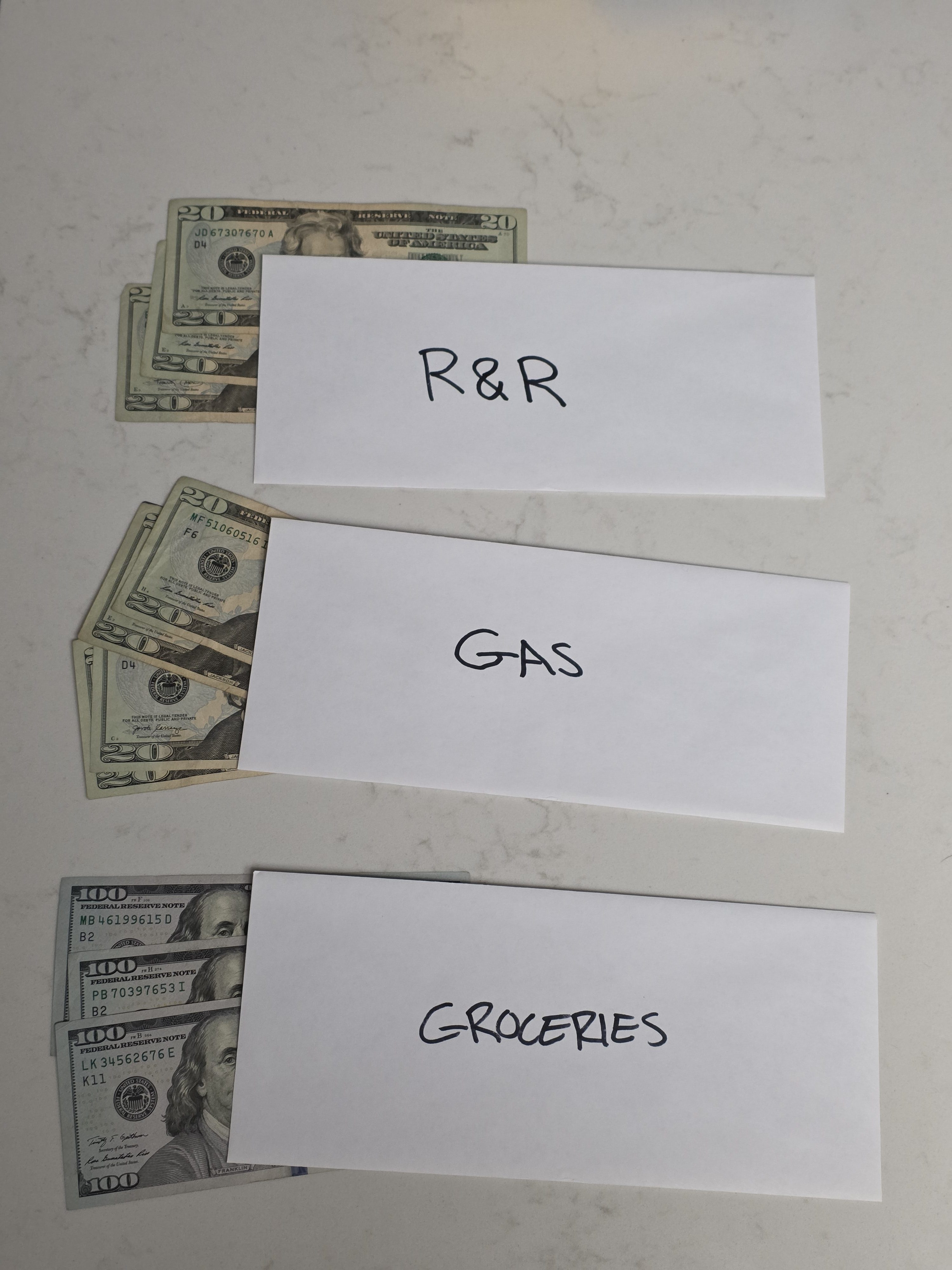

The System: 3 Envelopes

We still pay the mortgage, insurance, and utilities online using a modified version of the 50/30/20 rule. But for the “variable” stuff that actually fluctuates, we use a simple cash system. I withdraw the money at the start of the pay cycle and split it into three envelopes. No apps, no mental gymnastics.

- Groceries: This is the anchor. If we’re frugal in week one, we’ve got a choice: we either have a much nicer family dinner in week four, or we take that extra cash and throw it straight into our savings.

- Gas: This envelope stays in the car. At many stations, paying cash is still cheaper than credit. It’s a small win, but when you’re driving a family SUV every day, it adds up.

- R&R (Rest & Recreation): This is the fun money—trips to the park, movies, or treats. But there’s a hard rule: When the envelope is flat, the fun stops. We don’t “borrow” from the grocery fund to pay for a toy.

Why Friction Beats Cashback

People get hung up on 2% cashback and miss the bigger problem.

Using cash just hurts more—in a good way. When you see a $20 bill leave your hand, your brain registers it as a loss. When you tap a card, it doesn’t. That little bit of friction is usually enough to stop most dumb impulse buys.

This isn’t for everyone. If you’re a robot who never overspends and pays your balance in full every month, keep your points. But for the rest of us, my 18% in real-world savings beats 2% in rewards every single time. It isn’t even close.

If you’re tired of wondering where the paycheck went by the 10th of the month, try it for one pay cycle. Leave the cards in the drawer and use the envelopes. You’ll realize pretty quickly that you aren’t broke—you’re just “numb” to your own spending.

If you try this, give it one full pay cycle before you decide it doesn’t work.

Leave a Reply